The UK banking sector has reached a significant milestone in its financial contributions to the nation’s coffers, with recent figures revealing unprecedented tax payments that will have far-reaching implications for various segments of society. According to UK Finance’s 2024 banking sector tax report, prepared by PwC, the sector’s total tax contribution has soared to £44.8 billion for the financial year ending March 2024 – marking the highest figure since the study’s inception a decade ago.

Breaking Down the Numbers

This record-breaking contribution, up from £41 billion in the previous year, represents 4.7% of total UK government tax receipts. The figure comprises £24.1 billion in taxes borne (including corporation tax and bank levy) and £20.7 billion in taxes collected (including income tax and employee national insurance contributions). Notably, the sector contributed £10.8 billion in corporation tax and £24.9 billion in employment taxes, representing 12.2% and 5.9% of the government’s total tax receipts in these areas, respectively.

Impact on Different Sectors

For Pensioners:

- The increased tax contribution could potentially strengthen the government’s ability to maintain and possibly enhance pension payments

- The banking sector’s robust financial health might lead to better interest rates on savings accounts, particularly beneficial for retirees relying on interest income

- The stability indicated by these numbers could provide greater security for pension funds that invest in banking stocks

For Working Professionals:

- The high employment tax figure reflects the banking sector’s role as a major employer of skilled workers

- This could translate into continued job opportunities and competitive salaries in the financial sector

- The sector’s strong performance might lead to increased investment in training and development programs

For Small Business Owners:

- The banking sector’s financial strength could result in better lending conditions and more accessible business loans

- Enhanced financial services infrastructure might lead to improved banking services for SMEs

- However, the high tax burden on banks might indirectly affect banking fees and service charges

Global Competitiveness Analysis

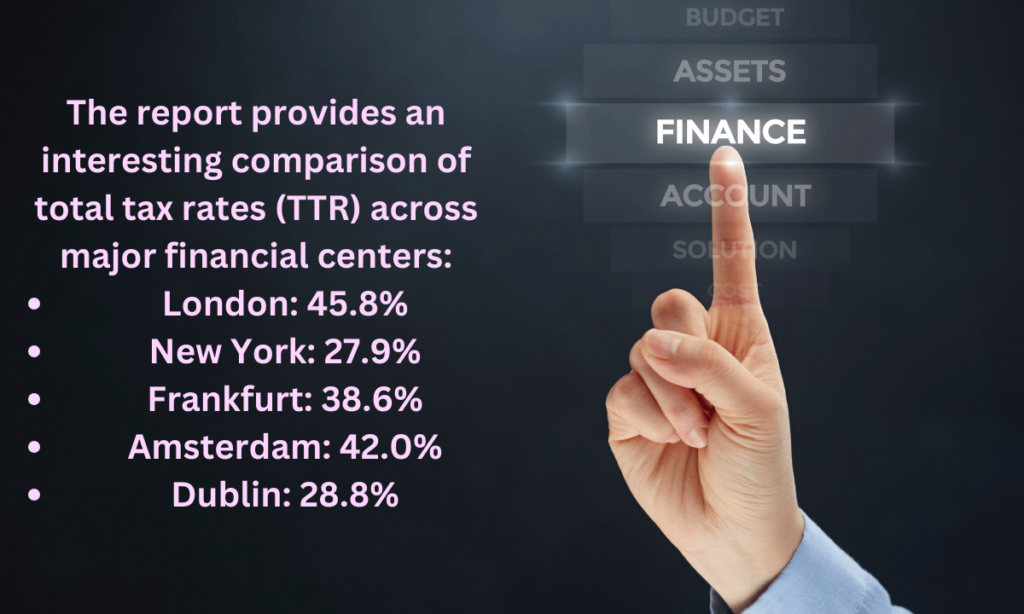

The report provides an interesting comparison of total tax rates (TTR) across major financial centers:

- London: 45.8%

- New York: 27.9%

- Frankfurt: 38.6%

- Amsterdam: 42.0%

- Dublin: 28.8%

This comparison reveals London’s significantly higher tax burden compared to other financial hubs, primarily due to the continued operation of the bank corporation tax surcharge and bank levy in the UK. This stands in contrast to the EU’s approach, where the Single Resolution Fund has already reached its target level.

Economic Implications

For the broader economy, these figures tell a compelling story:

- Strong Financial Sector: The increased tax contribution indicates a robust banking sector, essential for economic stability

- Employment Generation: The high employment taxes reflect the sector’s role in creating high-skilled, well-paid jobs

- Regional Development: As noted by David Postings, CEO of UK Finance, the sector supports skilled jobs across the country, contributing to regional economic growth

Future Outlook and Considerations

While these numbers demonstrate the banking sector’s significant contribution to the UK economy, they also raise important questions:

- Competitive Position:

- The higher tax burden in London compared to other financial centers might affect the UK’s attractiveness as a financial hub

- This could influence international banks’ decisions about their UK operations

- Consumer Impact:

- Banks might pass on some of their tax burden through adjusted service fees

- However, competition in the sector could help maintain reasonable consumer costs

- Economic Resilience:

- The strong tax contribution suggests a resilient banking sector

- This could provide a buffer against economic uncertainties

Recommendations for Different Groups

- For Pensioners:

- Consider reviewing savings accounts as banks might offer better rates

- Keep informed about banking sector stability for investment decisions

- For Working Professionals:

- Look for opportunities in the growing financial sector

- Consider upskilling to match the sector’s needs

- For Businesses:

- Monitor banking relationships and services

- Consider negotiating better terms based on the sector’s strong performance

Conclusion

The record-breaking tax contribution from the UK banking sector demonstrates its vital role in the nation’s economy. While the high tax burden compared to other financial centers raises competitiveness concerns, the sector’s robust performance suggests a strong foundation for continued growth and innovation. For individuals and businesses alike, understanding these developments is crucial for making informed financial decisions in an evolving economic landscape.

As David Postings emphasizes, financial services remain one of the UK’s key strengths, and this record tax contribution underscores the sector’s importance to both public finances and economic growth. Moving forward, balancing competitive taxation with maintaining the sector’s vital contribution to the UK economy will be crucial for sustained success.

Digital Banking Transformation and Its Effects

The significant tax contribution also reflects the banking sector’s ongoing digital transformation:

- Technology Investment:

- Banks are investing heavily in digital infrastructure

- This creates new job opportunities in fintech and digital banking

- Improved online services benefit all age groups, particularly younger customers

- Financial Inclusion:

- Digital banking makes financial services more accessible

- Reduced operational costs could lead to more competitive services

- However, concerns remain about maintaining services for less tech-savvy customers

Impact on Housing Market and Mortgages

The banking sector’s strong performance has important implications for the property market:

- Mortgage Availability:

- Strong bank profits could lead to more competitive mortgage products

- First-time buyers might benefit from innovative lending solutions

- Buy-to-let investors may see new opportunities

- Property Investment:

- Banks’ stability could support property market confidence

- Enhanced lending capacity might boost property development

- Potential for new property investment products

Environmental and Social Responsibility

The increased tax contribution also highlights the banking sector’s role in sustainable development:

- Green Finance:

- Banks are increasingly funding sustainable projects

- This creates opportunities for green investments

- Supports the UK’s net-zero targets

- Social Impact:

- Enhanced community investment programs

- Support for social enterprise lending

- Increased focus on financial education initiatives

Regional Economic Development

The banking sector’s contribution extends beyond London:

- Regional Employment:

- Growing presence in regional financial centers

- Creation of high-skilled jobs outside London

- Support for local economic development

- Local Business Support:

- Enhanced regional lending capabilities

- Support for local business growth

- Investment in regional infrastructure

International Trade and Brexit Implications

The tax contribution data provides insights into post-Brexit banking:

- International Competitiveness:

- Need to maintain London’s appeal despite higher tax rates

- Opportunity to develop new international partnerships

- Focus on innovation to offset tax disadvantages

- Trade Finance:

- Support for international trade

- Development of new cross-border services

- Enhanced global banking relationships

Future Trends and Predictions

Looking ahead, several key trends emerge:

- Digital Innovation:

- Continued investment in technology

- Enhanced customer service capabilities

- New financial products and services

- Regulatory Environment:

- Potential tax regime adjustments

- Enhanced focus on consumer protection

- Evolving international standards

Practical Guidelines for Different Groups

- For Young Professionals:

- Take advantage of digital banking innovations

- Consider career opportunities in fintech

- Monitor savings and investment options

- For Families:

- Review mortgage options regularly

- Consider new savings products

- Explore digital banking features for family finances

- For Retirees:

- Stay informed about branch banking services

- Explore assisted digital banking options

- Monitor savings rates and investment opportunities

- For Small Business Owners:

- Leverage new business banking technologies

- Explore green finance options

- Monitor international trading opportunities

Corporate Social Responsibility

The banking sector’s increased tax contribution reflects broader social responsibilities:

- Community Investment:

- Enhanced support for local communities

- Financial education programs

- Support for vulnerable customers

- Environmental Initiatives:

- Green lending programs

- Sustainable investment options

- Carbon reduction commitments

Policy Implications

The tax contribution data suggests several policy considerations:

- Tax Policy:

- Balance between competitiveness and fair contribution

- Support for regional development

- International tax coordination

- Financial Regulation:

- Consumer protection measures

- Digital banking standards

- International cooperation

Recommendations for Stakeholders

- Government:

- Monitor international competitiveness

- Support regional development

- Enhance digital infrastructure

- Banking Sector:

- Continue innovation investment

- Maintain customer service focus

- Develop sustainable practices

- Consumers:

- Stay informed about banking changes

- Review financial products regularly

- Consider digital banking adoption

- Businesses:

- Explore new banking technologies

- Consider green finance options

- Monitor international opportunities

Conclusion

The UK banking sector’s record £44.8 billion tax contribution represents more than just a financial milestone. It reflects a sector undergoing significant transformation while maintaining its position as a crucial contributor to the UK economy. The higher tax burden compared to other financial centers presents challenges, but also demonstrates the sector’s resilience and capacity for innovation.

For individuals, businesses, and communities across the UK, the banking sector’s strong performance offers both opportunities and responsibilities. Whether through digital innovation, sustainable finance, or regional development, the sector’s contribution extends far beyond its tax payments.

As we look to the future, the balance between maintaining international competitiveness and ensuring fair contribution to public finances will remain crucial. The sector’s ability to adapt to changing circumstances while supporting economic growth and innovation will be key to its continued success.

The challenge now is to build on this strong foundation, ensuring that the benefits of a robust banking sector continue to support economic growth and social development across the UK. This requires ongoing collaboration between government, industry, and stakeholders to create an environment that promotes innovation, sustainability, and inclusive growth while maintaining the UK’s position as a leading global financial center.